Security continued improving using public-key cryptography, but as technology also advanced, new trust problems cropped up with the advent of the internet. By 1992, a group of cryptographers calling themselves the Cypherpunks created an email mailing list where they discussed their ideas and experiments in cryptography as they tried to solve information security issues. Among the members of the Cypherpunks were Julian Assange, Bram Cohen, who created BitTorrent, and many of the people who pioneered early iterations of digital currencies.

Security continued improving using public-key cryptography, but as technology also advanced, new trust problems cropped up with the advent of the internet. By 1992, a group of cryptographers calling themselves the Cypherpunks created an email mailing list where they discussed their ideas and experiments in cryptography as they tried to solve information security issues. Among the members of the Cypherpunks were Julian Assange, Bram Cohen, who created BitTorrent, and many of the people who pioneered early iterations of digital currencies.

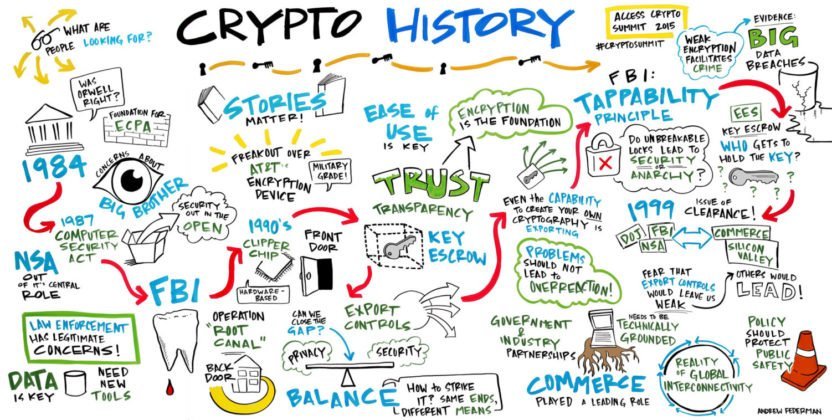

The Cypherpunks were concerned with privacy, having a strong distrust of governments and corporations, which are typically the gatekeepers of information and finances. These privacy rebels were not willing to give any ground to the government, even though exporting cryptographic technology was illegal and considered the export of munitions until the early 1990s. The argument over national security versus privacy became known as the Crypto Wars and, in many ways, it continues today.

Out of the ranks of Cypherpunks came a slew of coders who created important predecessors to modern cryptocurrencies. All of them contributed valuable pieces to the puzzle that Nakamoto solved with Bitcoin. Let’s talk about some of those solutions.

Coders and crypto enthusiasts were among the first groups to begin using Bitcoin and as more people began mining Bitcoins, they also started trading them. In 2010, Laszlo Hanyecz paid for two pizzas with 10,000 Bitcoins. This was the first real-world purchase using the cryptocurrency and effectively set a price relative to the dollar. Assuming two pizzas were worth roughly $41, one Bitcoin would have been worth about $0.004.

Coders and crypto enthusiasts were among the first groups to begin using Bitcoin and as more people began mining Bitcoins, they also started trading them. In 2010, Laszlo Hanyecz paid for two pizzas with 10,000 Bitcoins. This was the first real-world purchase using the cryptocurrency and effectively set a price relative to the dollar. Assuming two pizzas were worth roughly $41, one Bitcoin would have been worth about $0.004.

Bitcoin’s decentralized nature made it pretty much impossible to control or censor. This opened the door for Ross Ulbricht and the darknet’s Silk Road, which allowed Bitcoin to be used as currency to buy and sell things on the black market. This marketplace lasted from 2011 to 2013, when Ulbricht was arrested. Julian Assange and WikiLeaks also used Bitcoin in the early 2010s to weather its US banking blockade, when WikiLeaks was ejected from centralized payment platforms.

Those paying attention quickly began to see the usefulness of Bitcoin and decentralized, trustless currency. It soon reached parity with the dollar in 2011—just a couple of years after its creation—and in the ensuing decade, despite wild swings of volatility, Bitcoin rocketed to a temporary all-time high of $64,899 in April of 2021.

Trading exchanges began to emerge thanks to the increased use of cryptocurrency, and in 2014, Mt. Gox was the largest exchange. However, it was investigated by the US Department of Homeland Security for not having proper registrations and it was also hacked, which resulted in the loss of 744,408 Bitcoins. By February 28, 2014, Mt. Gox was bankrupt, and many Bitcoin holders learned a difficult lesson about the importance of keeping custody of their crypto.