It doesn’t matter how massive the hype; there’s always a limit where the “new thing” goes too far. NFTs have been a red hot commodity over the past year, but it looks like the trend might be cooling off. Even though more money is pouring into NFTs than ever before, there’s something to be said for understanding when corporations are hopping on a trend—well—JUST to hop on, and nothing more.

We reported previously that TikTok was going to get in on the NFT action with none other than music megastar Lil Nas X, but it looks like things are getting rocky. How, you ask? Well, one massive problem is that the NFT never dropped. On top of that, Bella Poarch is apparently thinking about pulling out of the program, and this is AFTER a Lil Uzi Vert-related NFT scandal.

The “Macarena” was massive, but it had its moment. These scandals could potentially mean that the average investor begins viewing NFTs as a “fad” rather than a real sector, the same way that we all collectively decided that a summer anthem outlasted its stay, or that a TV show is more cringeworthy than we’d like to admit. The TikTok NFT partnership already appears to be flopping, and TikTok is one of the most popular apps in the world.

These are problems that don’t even take into account the environmental concern surrounding NFTs. Will this affect the NFT market moving forward, or not really?

It wasn’t too long ago that many traditional financial institutions were downplaying Bitcoin, or arguing that cryptocurrencies would never be that much of a factor in finance. It seems as though all of them are singing quite a different tune these days. In fact, they seem to be going out of their way to let potential clients know that they are researching the space.

Bank of America is apparently now releasing crypto reports. They aren’t the only financial company interested in diving into crypto, either. Apparently, Visa sees massive potential in a future “universal payment channel” across interconnected blockchain networks. As if that wasn’t enough, apparently even Morgan Stanley wants to get in on the action. Is this important cryptocurrency news or just a corporate cash-grab?

It might feel satisfying to actually SEE Bank of America admit that crypto is “too large to ignore,” but will they actually bring any value to the sector? In a sector that values decentralization, is there REALLY a place for these corporations?

In a world where global business has had to deal with the wrath of an unrelenting pandemic, there’s been some good cryptocurrency news. There are now six new crypto billionaires on the Forbes 400 list, with a combined wealth of somewhere around $55.1 billion dollars. These six individuals have landed on the list of the nation’s richest people. Check back for new profiles we’re releasing on crypto billionaires.

The billionaires are not too surprising to anyone who follows the cryptocurrency sector closely. The six include Brian Armstrong and Fred Ehrsam, co-founders of Coinbase. Coinbase is one of the largest and most influential cryptocurrency companies in the world. Jed McCaleb also joined the list, who is famous for founding Mt. Gox, an early cryptocurrency exchange that was hacked and closed down in 2014.

Forbes remains one of the most prestigious business publications in the world, and they are world-renowned for their “lists” specifically. While these new additions might not single handedly lead to massive retail investor interest, it does help to legitimize the sector and bring in new eyeballs and investors that may not otherwise be interested.

For those who don’t know, Edward Snowden is arguably the most famous whistleblower in the world. A former NSA agent, Snowden leaked documents regarding various global surveillance programs. He is a polarizing figure, with many Americans divided over whether Snowden was justified in revealing classified documents, even if it exposed illegal and/or unconstitutional activity.

Whether you like him or not, Snowden’s opinion on anything technology-related is bound to hold weight. Some Americans view Snowden as a modern hero of our times, thankful for the fact that he exposed global surveillance programs that the government didn’t know about. Others feel like Snowden betrayed his country, or should come back to America to face his charges. For crypto enthusiasts, you can count this as overall positive cryptocurrency news.

Snowden tweeted on October 3, 2021, pointing out that Bitcoin was up around “10x” since a March 2020 tweet where he claimed that he was interested in buying the cryptocurrency for the first time. Snowden pointed out that Bitcoin was resilient, even despite the recent China crypto ban.

While this might not be monumental cryptocurrency news, the fact that Snowden is now pro-crypto is probably a net positive for the crypto markets.

Well, well, well.

Well, well, well.

It appears as though officials at the Federal Reserve want to study whether creating its own digital currency is a smart move. On behalf of Decentral, I’d like to honor the Fed with the “Late to the Party” award. This is also apparently a passive-aggressive party, considering Jerome Powell was bashing cryptos several months ago, suggesting they were mere vehicles for speculation. Now, they’re thinking about launching a CBDC (central bank digital currency).

It’s strange to think that the Fed suddenly believes that ITS version of cryptocurrency is valid, given the fact that the existence of a federal reserve isn’t something that many cryptocurrency die-hards are excited about. The Fed has been exploring the concept of a digital dollar for some time now, and this certainly doesn’t mean that they are embracing crypto—as much as trying to see how they can make blockchain technology work for their purposes.

Many crypto investors would argue that the Federal Reserve and the crypto sector are at odds, given that one is a centralized institution and the other sector hopes to emphasize the importance of decentralization.

Is this just a means to try to control or regulate the sector?

How’d you like to live in a castle? That’s right. There’s a private hospital that claims to be the first center in the world to treat cryptocurrency addiction, and it’s run out of

How’d you like to live in a castle? That’s right. There’s a private hospital that claims to be the first center in the world to treat cryptocurrency addiction, and it’s run out of  As both novice and expert crypto traders know, Bitcoin’s price determines a lot in the cryptocurrency markets. This is one reason why many experts were concerned that Bitcoin had dipped down—twice—near the

As both novice and expert crypto traders know, Bitcoin’s price determines a lot in the cryptocurrency markets. This is one reason why many experts were concerned that Bitcoin had dipped down—twice—near the  Facebook is one of the most powerful tech companies in the world, but it has been having a terrible week. First, Facebook, Instagram, and Whatsapp

Facebook is one of the most powerful tech companies in the world, but it has been having a terrible week. First, Facebook, Instagram, and Whatsapp  What happens when one of the hottest “crypto trends” in cryptocurrency news teams up with the “trendiest” platform, famous for challenges, dances, and teenage discourse? You’ve guessed it: NFTs are coming to TikTok!

What happens when one of the hottest “crypto trends” in cryptocurrency news teams up with the “trendiest” platform, famous for challenges, dances, and teenage discourse? You’ve guessed it: NFTs are coming to TikTok!  Last week, we spoke about how El Salvador was embracing Bitcoin, and how the president of El Salvador, Nayib Bukele, seems to believe that Bitcoin will play a critical role in improving the country’s economy. Bukele, who many consider to be authoritarian and

Last week, we spoke about how El Salvador was embracing Bitcoin, and how the president of El Salvador, Nayib Bukele, seems to believe that Bitcoin will play a critical role in improving the country’s economy. Bukele, who many consider to be authoritarian and

Well, chances are the adoption train will keep chugging in the next year.

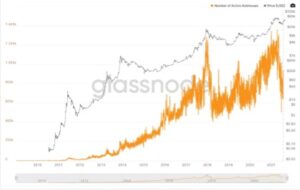

Well, chances are the adoption train will keep chugging in the next year. The number of active Bitcoin addresses has been steadily climbing, as well, almost doubling between January of 2020 and April of 2021. Active addresses are volatile, just like the price of Bitcoin, and have dipped in the second half of 2021, but the trend continues upward on the whole. In fact, by the time you read this article, Bitcoin will have reached another all-time high.

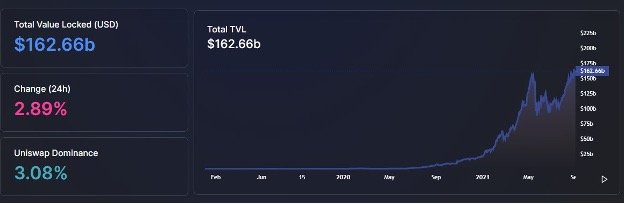

The number of active Bitcoin addresses has been steadily climbing, as well, almost doubling between January of 2020 and April of 2021. Active addresses are volatile, just like the price of Bitcoin, and have dipped in the second half of 2021, but the trend continues upward on the whole. In fact, by the time you read this article, Bitcoin will have reached another all-time high. The summer of 2020 was a huge DeFi extravaganza as investment dollars flowed into the ecosystem, and in August, asset value was growing by nearly half a billion dollars a week. In the ensuing year, DeFi continued to explode and by August of 2021, it had more than $160 billion total value locked (TVL). This growth is expected to continue into 2022 as more new projects get off the ground.

The summer of 2020 was a huge DeFi extravaganza as investment dollars flowed into the ecosystem, and in August, asset value was growing by nearly half a billion dollars a week. In the ensuing year, DeFi continued to explode and by August of 2021, it had more than $160 billion total value locked (TVL). This growth is expected to continue into 2022 as more new projects get off the ground. If you’ve been following cryptocurrency news for a while, you may not be too surprised to find out that China has recently

If you’ve been following cryptocurrency news for a while, you may not be too surprised to find out that China has recently  Since we started off with some bad news, let’s move on to something more fun: a hamster that is better at managing their portfolio than you may be. That would be the cryptocurrency trading hamster, Mr. Goxx, who lives on Twitch and has captured the hearts of many crypto traders. The hamster already boasts

Since we started off with some bad news, let’s move on to something more fun: a hamster that is better at managing their portfolio than you may be. That would be the cryptocurrency trading hamster, Mr. Goxx, who lives on Twitch and has captured the hearts of many crypto traders. The hamster already boasts  For those new to the cryptocurrency space, a crypto mystery has plagued the community for years. What

For those new to the cryptocurrency space, a crypto mystery has plagued the community for years. What  It might not have been publicized that much, but there’s something different about Twitter. Yes, the

It might not have been publicized that much, but there’s something different about Twitter. Yes, the  Several weeks ago, there was a huge milestone for countless cryptocurrency enthusiasts: a country

Several weeks ago, there was a huge milestone for countless cryptocurrency enthusiasts: a country  There are several stablecoins out there, and they serve a real purpose for the DeFi sector. However, all stablecoins are not necessarily equal in the eyes of the cryptocurrency investor. Tether has had all sorts of issues, with some critics calling it

There are several stablecoins out there, and they serve a real purpose for the DeFi sector. However, all stablecoins are not necessarily equal in the eyes of the cryptocurrency investor. Tether has had all sorts of issues, with some critics calling it